For natural gas and electricity buyers across the Northeast, winter 2026 was defined by Winter Storm Fern. The storm hit the region in late January and brought a cold snap filled with operational challenges. During that window, daily spot prices for natural gas, the rates set by the market each day for next-day delivery, reached some of the highest levels ever recorded for this part of the country. Electricity prices followed, as both pipelines and the grid ran up against their physical limits.

This post covers what happened, why the Northeast market reacts the way it does to extreme cold, and what businesses can do to reduce their exposure to this kind of volatility in the future.

Why Fern Was Different

A few factors stacked up at the same time during Winter Storm Fern.

Prolonged subfreezing temperatures across a wide geography pulled heating demand up sharply, not just in the Northeast but in the gas-producing regions to the south and west. In several of those producing regions, extreme cold led to “freeze-offs,” where water and other liquids in natural gas systems freeze and block wells, pipelines, and compressor equipment. At the peak, freeze-offs knocked roughly 18 billion cubic feet per day of production offline across the Lower 48. To make up for lost supply, storage withdrawals jumped sharply.

The Northeast was hit especially hard because of how the regional system is built. Pipelines into New England and the Mid-Atlantic run near full capacity during any serious cold snap. When more gas is needed, there is no extra pipe space to bring it in, so regional prices rise in attempts to balance the system. No new major pipelines are scheduled to come online in 2026 or 2027, which means this is an ongoing structural risk, not a one-time instance. With demand surging, supply constrained, and pipeline capacity maxed out, the market became extremely volatile.

At the same time, global demand for U.S. natural gas remained strong. LNG export facilities continued to pull significant volumes of gas out of the domestic market to meet international demand, particularly as geopolitical tensions kept global energy markets tight.

That additional demand doesn’t typically drive price spikes on its own. But it does reduce the amount of excess supply available in the system by linking more U.S. gas to global demand. When a weather event like Fern hits, there is less flexibility to absorb the shock, which can amplify price movements. Ongoing LNG export demand and global market pressures mean the system has less flexibility than it once did, which can keep upward pressure on costs during future periods of stress.

The Ten Days That Defined the Winter

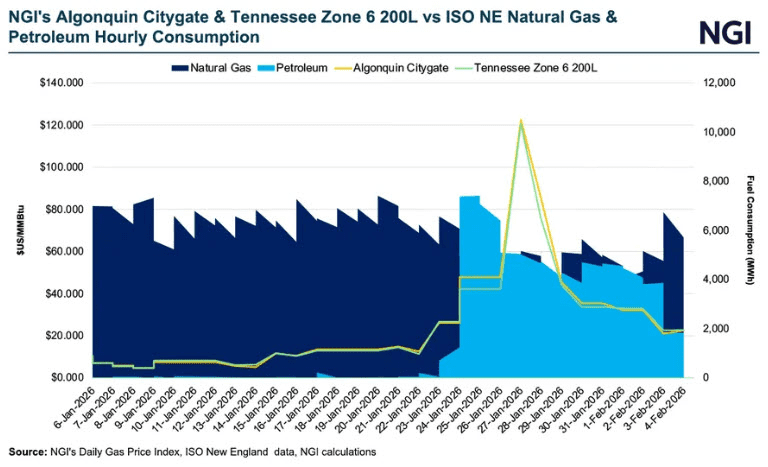

While January and February were cold, they were not historic. The real story was a concentrated ten-day cold snap, roughly January 23 through February 2, that pushed heating demand to extreme levels day after day.

A few numbers from that window:

- Algonquin Citygate, the main pricing hub for natural gas delivered into the Greater Boston area, averaged above $35 per MMBtu from January 24 through January 31. For context, Citygate averaged around $8-$10 for much of the Northeast in January.

- On January 26, Algonquin Citygate hit $122.575 per MMBtu. PNGTS soared $48.785 to $73.335, while Maritimes & Northeast surged $77.380 to $90.360.

- By February 1, real-time power prices in New England spiked to $400 to $700 per megawatt-hour. Electricity tracks gas in New England because natural gas plants typically set the price for power on the regional grid, so when gas prices climb, electricity prices tend to climb with them.

[Source: https://naturalgasintel.com/news/winter-storm-fern-exposes-northeast-supply-constraints-sends-natural-gas-prices-soaring/ February 6, 2026]

These prices are many times what a typical commercial buyer plans for in their winter budget. A business taking gas during the last week of January paid a multiple of what they paid the prior week, on volumes that were themselves higher because of the cold.

The contrast with the rest of the country was stark. The 2025 to 2026 winter was one of the warmest on record nationally, and Southwest natural gas prices stayed low through the storm. The gap between regional and national prices is what the gas industry calls a basis blowout. Basis is the difference between the price at a regional hub like Algonquin Citygate and the national benchmark price set at Henry Hub, a major hub in Louisiana. In mild months, Algonquin trades within pennies of Henry Hub. During Fern, that gap widened to levels rarely seen. During Fern, that gap widened to levels rarely seen.

For regulated utilities, price spikes like these don’t always show up immediately in customer rates, but they often surface later as utilities work to recover their actual supply costs.

What This Meant for Market-Based Buyers

If you purchase natural gas or electricity on the open market without a contract, your rate floats with daily spot prices. In a mild winter, that can work in your favor. In a winter with a concentrated cold snap like Fern, you are fully exposed to the kind of price moves shown above.

The Northeast burns most of its gas on the coldest days. Because cold-day usage is concentrated, those days end up driving a disproportionate share of a market-based buyer’s winter bill. The math typically works against floating rates exactly when usage is likely to be the highest.

Market-based pricing is a legitimate approach. Sprague has many customers on contracts that float fully or partially with the market, and there are good reasons to choose that structure. But Winter Storm Fern is a useful moment to talk about an alternative for buyers whose priority is limiting market-price exposure. A fixed-price contract can shield you from that exposure.

A fixed-price contract locks in your rate for the contract term, regardless of what the market does. The basis premium and the underlying commodity price are both set in advance. Depending on how the contract is structured, you can choose to fully eliminate market exposure or accept a small amount of risk on usage above your expected volume. Either way, the bulk of your winter pricing is set before the season starts.

There are other contract structures available for buyers who want a partial hedge or more flexibility, but if your goal is the most direct protection against a Fern-style event, a full fixed-price program is the cleanest path.

What This Could Mean for Utility Rates

Regulated utilities in the Northeast and Mid-Atlantic absorbed significant supply cost overruns during Fern. During the coldest stretch, utilities were buying gas at elevated daily market prices while still charging customers based on previously set rates.

That gap between what utilities paid and what they collected creates a deferred cost balance. Those costs don’t disappear. They are typically recovered in future rate adjustments, which is why events like Fern often show up in customer bills months later.

In some cases, utilities have already raised rates to begin recovering those costs. In others, seasonal rate resets may temporarily lower prices, even while underlying balances are still being worked through.

Because each state and utility follows its own regulatory process, the timing and magnitude of these adjustments can vary. But the underlying dynamic is consistent: when costs spike during the winter, recovery often extends into future rate periods.

As utilities continue to reconcile winter 2026 costs and set new rates for the next cycle, additional adjustments later this year remain a real possibility.

What Business Can Do

Sprague has been supplying energy across the Northeast since 1870. We have worked through energy crises, pipeline constraints, extreme weather, and geopolitical shocks going back generations. If winter 2026 raised questions about your approach to natural gas or electricity procurement, reach out to your Sprague representative. We can walk through what a fixed-price contract would look like for your business and help you think about what fits heading into next winter.